Debt is a reality that touches nearly every household at some point. Whether it comes in the form of credit cards, personal loans, mortgages, or unforeseen expenses, debt can create stress, reduce financial freedom, and disrupt family life. For many, it can feel like a flood slowly creeping into every corner of the home, leaving behind anxiety, tension, and limited financial options.

Preventing debt flooding starts with awareness, planning, and disciplined action. By understanding the causes, implementing practical strategies, and fostering a healthy financial mindset, families can protect their homes and financial futures from overwhelming debt. This comprehensive guide explores why debt can be bothersome and how to prevent it from taking over your home.

Understanding Household Debt

1. What Constitutes Household Debt?

Household debt includes all obligations owed by members of a household. Common types include:

- Credit Card Debt – Often high-interest and revolving, leading to growing balances if not managed.

- Personal Loans – Fixed-term borrowings for personal needs or emergencies.

- Mortgages – Long-term loans for property purchase.

- Auto Loans – Financing for vehicles, which depreciate quickly.

- Student Loans – Education-related debt, often with deferred repayment schedules.

Understanding all sources of debt is the first step in preventing it from overwhelming your home.

2. Why Debt Can Be Bothersome

- Stress and Anxiety – Constant worry about payments or interest accumulation.

- Reduced Financial Freedom – Less ability to save, invest, or spend on essentials.

- Family Tension – Disagreements over money can strain relationships.

- Long-Term Financial Risk – High-interest debt can grow faster than income.

Debt becomes especially troublesome when it is unmanaged, excessive, or unplanned.

Causes of Debt Flooding

Understanding the root causes of household debt is essential for prevention:

1. Overspending

- Living beyond your means leads to accumulating balances.

- Frequent use of credit cards for non-essential purchases increases vulnerability.

2. Lack of Budgeting

- Without a clear plan for income and expenses, debt can accumulate unnoticed.

- Impulse purchases, irregular bills, and unexpected expenses can contribute to debt buildup.

3. Emergencies and Unplanned Expenses

- Medical bills, car repairs, or home maintenance costs can trigger debt if no emergency fund exists.

- Reliance on credit rather than savings amplifies debt risk.

4. High-Interest Debt

- Credit cards and payday loans often carry extremely high interest rates.

- Minimum payments can prolong repayment and increase total debt.

5. Insufficient Financial Education

- Lack of knowledge about interest rates, compounding, and repayment strategies contributes to poor financial decisions.

- Misunderstanding financial products increases vulnerability.

How to Prevent Debt Flooding

Preventing debt flooding requires proactive planning, awareness, and disciplined action.

1. Create a Household Budget

A detailed budget is the cornerstone of financial health:

- List all sources of income.

- Track all fixed and variable expenses.

- Allocate funds for necessities, savings, and discretionary spending.

- Review monthly and adjust based on real spending patterns.

A budget creates clarity, reduces overspending, and identifies areas where debt can be avoided.

2. Build an Emergency Fund

An emergency fund acts as a financial buffer:

- Save at least 3–6 months of living expenses.

- Use the fund only for genuine emergencies.

- Reduces reliance on credit cards or loans during unexpected events.

This fund prevents small emergencies from escalating into long-term debt.

3. Avoid Unnecessary Borrowing

- Differentiate between essential and non-essential purchases.

- Delay gratification for non-urgent purchases.

- Use cash or debit cards instead of credit when possible.

Resisting unnecessary borrowing reduces the chance of debt accumulation.

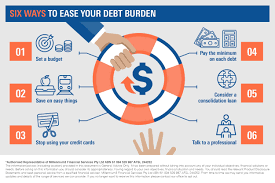

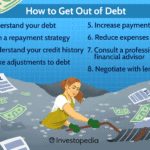

4. Manage Existing Debt Strategically

- Pay High-Interest Debt First – Focus on cards or loans with the highest interest rates.

- Consolidate Debt – Combining multiple debts into a single loan with lower interest can simplify payments.

- Negotiate with Creditors – Sometimes repayment terms or interest rates can be adjusted.

A strategic approach prevents debt from snowballing.

5. Monitor Your Credit and Spending

- Regularly check credit card statements and account balances.

- Track recurring payments and automatic charges.

- Stay informed about your credit score and financial standing.

Monitoring ensures early detection and prevents unnoticed debt growth.

Financial Mindset and Habits

1. Practice Financial Discipline

- Spend less than you earn consistently.

- Avoid impulse purchases.

- Prioritize saving and debt repayment.

2. Educate Yourself Financially

- Understand interest rates, compounding, and credit terms.

- Learn about investment and saving options to grow wealth responsibly.

3. Set Clear Financial Goals

- Short-term goals: Save for a vacation, emergency fund, or debt repayment.

- Long-term goals: Home purchase, retirement planning, or education fund.

- Goals create motivation and reduce unnecessary borrowing.

4. Encourage Family Participation

- Discuss budgets, spending habits, and financial priorities with family members.

- Collective awareness prevents overspending and strengthens financial responsibility.

Practical Tips to Maintain a Debt-Free Home

- Use Cash Envelopes – Allocate specific amounts for groceries, entertainment, and discretionary spending.

- Automate Savings – Set up automatic transfers to savings or investment accounts.

- Track Every Expense – Even small purchases add up; tracking prevents unnoticed debt.

- Limit Credit Card Usage – Keep one primary card for emergencies and essentials.

- Plan for Major Expenses – Save for vacations, holidays, and large purchases instead of borrowing.

- Review Subscriptions – Cancel unused memberships or automatic services.

- Live Below Your Means – Avoid lifestyle inflation even if income increases.

The Role of Communication

Open communication about finances is essential to prevent debt flooding:

- Discuss money matters with partners or household members.

- Agree on spending limits and priorities.

- Review monthly financial statements together.

- Address potential debt issues early before they escalate.

Effective communication reduces stress, prevents misunderstandings, and creates a proactive financial culture.

Preparing for Unexpected Debt

Even with careful planning, unexpected debt may arise:

- Insurance – Health, auto, home, and life insurance protect against major financial shocks.

- Side Income – Part-time work or freelance projects can supplement income during emergencies.

- Debt Repayment Plans – Negotiate structured repayment if unavoidable debt occurs.

Preparation ensures that emergencies do not flood your home with debt.

Psychological and Emotional Benefits

Preventing debt flooding improves not only finances but also emotional well-being:

- Reduces stress and anxiety.

- Improves sleep and mental clarity.

- Strengthens family relationships.

- Creates a sense of control and security.

Debt prevention is as much about mental peace as financial stability.

Long-Term Strategies for Financial Security

- Invest for Growth – Use long-term investments to build wealth instead of relying on borrowing.

- Maintain Good Credit – Responsible use of credit ensures access to favorable loans if needed.

- Review Financial Goals Annually – Adjust savings, budgets, and repayment plans according to changing circumstances.

- Seek Professional Advice – Financial planners or counselors can provide personalized strategies.

Long-term planning ensures sustained financial health and reduces the risk of debt flooding.

Conclusion

Debt can indeed be bothersome, creeping into every corner of a household and creating stress, tension, and financial instability. However, with proactive strategies, disciplined habits, and a strong financial mindset, families can prevent debt flooding and maintain a secure, peaceful home environment.

Key takeaways include:

- Understand the sources and causes of debt.

- Create and follow a detailed household budget.

- Build an emergency fund to handle unexpected expenses.

- Manage existing debt strategically and avoid unnecessary borrowing.

- Develop disciplined financial habits and involve family members.

- Plan for long-term financial security and investment.

By applying these principles, households can protect themselves from debt, enjoy financial peace, and create a foundation for lasting prosperity.

Debt problems exist all around the map and most families find themselves struggling over one thing or another at some point in time, it is a sad but very true problem going on in the world. Debt can be and is very bothersome, so for anyone out there who is finding a hard time getting out of the debt that you are in, please do continue reading this entire article, hopefully it will be more than helpful to you all.

Anytime that somebody offers a word of advice, you should always take the time out to listen up because you might just find that it is very helpful advice. There are many professionals available to anyone out there needing any sort of debt assistance, and by choosing to go with a professional you can be assured that you are going to be all set up and placed on the correct path for a successful financial future.

Debt problems will send you in a spiral of frustration, anxiety and even depression at times, so knowing what not to do with your money is really very important. Debt consolidation is always an option to help anyone who is in financial assistance and if you find yourself drowning in debt then perhaps you should definitely be considering some different options that could help to straighten you all out.

Consolidating your bills each month will make it possible for you to save yourself some money every chance that you get and by doing so you are always going to have a little bit of extra money in the bank each month that comes along. Your extra money can be put into some sort of stocks or cd’s, perhaps you could start seeing that you do know how to save more money each month, it might even be quite shocking to you at first.

Debt flooding within your home can be very exhausting for anyone responsible for trying to correct the current situation within the home. It can be extremely tiring and overwhelming just trying to find any sort of answer that could potentially help to get you through this horrifying time in your life. It is real important for you to pick up some helpful books regarding debt because if you do not do something now about this problem, things are going to become very bothersome and even more of a headache than ever before.

Your life does not have to be this way, making a few more intelligent decisions when it comes to your money each month, will truly provide you with the type of financial stability that you are looking for and have been looking for now for quite some time and have not yet been successful with any type of action. Get a friend that you can trust that might know a bit more about debt flooding and all of the problems that can come from having to deal with it. Good luck!

Tinggalkan Balasan