Tool To Eliminate DebtBy [Bhara.s], CEO and Financial Strategist-In a world defined by opportunity, innovation, and constant change, one quiet adversary has continued to grow in the shadows: debt. Across every economy and social class, debt has evolved from a temporary financial tool into a pervasive barrier to freedom, creativity, and growth. It limits choices, constrains innovation, and silently erodes human potential.But what if we could treat debt not as a life sentence, but as a solvable equation?What if the same strategic thinking that drives successful businesses could be applied to personal finance?This is where the concept of “A Tool To Eliminate Debt” emerges — not merely as software or a calculator, but as a mindset, a strategy, and a disciplined framework for transforming financial stress into sustainable success.

- The Modern Debt Dilemma

-Debt is not new. It has existed as long as trade and credit have. Yet, the psychology of debt today is unprecedented. Easy access to credit cards, online loans, and “buy now, pay later” options has redefined how people view borrowing. Debt no longer feels heavy or risky — until it’s too late.

For many, debt begins innocently. A small balance here, a short-term loan there. But compounded interest, delayed payments, and emotional spending habits can quickly turn a few hundred dollars into a lifelong burden. This is not a failure of intelligence — it’s a failure of systems, habits, and awareness.

In corporate terms, we could call this a “cash flow mismanagement problem.”

But for individuals, it’s deeper — it’s behavioral economics meeting human emotion.

The truth is: debt is not just a financial issue; it’s a behavioral one. - The Leadership Perspective on Debt

-As leaders, we often discuss efficiency, scalability, and sustainability. We set targets, monitor metrics, and manage resources strategically. Yet when it comes to our own finances, we often abandon those same principles. Personal finance management, for many executives and entrepreneurs, becomes reactive instead of strategic.

A leader who runs a company with perpetual losses would not survive long. But millions of people “run their personal economies” that way every day — spending more than they earn, borrowing to fill gaps, and hoping for a raise or windfall to fix it later.

-Debt elimination, then, is not just about numbers. It’s about adopting a CEO mindset toward one’s personal financial life. Every individual should think of themselves as the Chief Executive Officer of their own economy — responsible for income growth, expense control, risk management, and strategic reinvestment.

This is the essence of A Tool To Eliminate Debt: a structured, executive-style approach to personal finance management.

- What Is “A Tool To Eliminate Debt”?

-At its core, “A Tool To Eliminate Debt” represents an integrated framework that combines technology, psychology, and strategy to empower individuals to regain financial control. It is both a philosophy and a practical system, designed to turn the abstract idea of “being debt-free” into a concrete, achievable mission.

The tool consists of five foundational pillars:

Awareness – Understanding every aspect of one’s debt, from interest rates to emotional triggers.

Analysis – Strategically prioritizing debts based on mathematical efficiency (interest rates) or psychological momentum (small wins).

Action – Implementing a disciplined repayment plan with automation and measurable goals.

Adaptation – Adjusting the plan as income, expenses, and circumstances evolve.

Accountability – Tracking progress transparently, celebrating milestones, and maintaining consistency.

These principles mirror the way successful companies operate. Just as corporations use dashboards, performance metrics, and forecasting tools, individuals too can build their own financial command centers — powered by insight and discipline. - The Technology Behind Debt Freedom

-Technology has democratized finance. Apps, digital wallets, AI-driven budgeting platforms, and smart analytics now allow anyone to visualize and optimize their financial landscape. However, technology alone is not the solution — it’s an enabler.

“A Tool To Eliminate Debt” leverages digital innovation to make financial management seamless, yet deeply human. Imagine an intelligent assistant that not only tracks your expenses but also anticipates risk, recommends repayment strategies, and rewards consistency.

Key features of a truly effective debt elimination tool include:

Debt Mapping: Visual representation of all debts, categorized by type, rate, and priority.

Interest Forecasting: Predicting total interest over time to emphasize the cost of inaction.

Smart Repayment Plans: Algorithms that optimize payment sequences for maximum savings.

Behavioral Nudges: Reminders and motivational cues to sustain engagement.

Gamified Progress Tracking: Celebrating each milestone to create emotional reinforcement.

The future of personal finance lies in behavioral technology — tools that understand not only our wallets but our minds. The right tool doesn’t just manage your debt; it transforms your relationship with money. - Behavioral Economics: The Hidden Battle

-Every debt problem begins in the mind before it appears in the numbers. Behavioral economics teaches us that people don’t always act rationally with money. We are emotional beings — influenced by fear, gratification, and social comparison.

The average person knows they shouldn’t spend more than they earn, yet millions still do. Why? Because financial decisions are rarely logical; they are emotional responses to unmet needs or pressures.

A Tool To Eliminate Debt integrates behavioral awareness into its strategy. By recognizing triggers such as stress spending, impulse buying, and lifestyle inflation, it helps users rewire their habits. Just as athletes train their bodies, individuals must train their financial discipline muscles.

The process begins with awareness — identifying emotional patterns that lead to debt accumulation. Then comes accountability — creating systems that prevent those behaviors from repeating. Over time, consistency turns discipline into freedom.

- The Financial Freedom Framework

-To eliminate debt effectively, individuals need more than hope — they need a framework. “A Tool To Eliminate Debt” outlines a five-phase roadmap that mirrors corporate transformation strategies.

Phase 1: Audit and Awareness

Every CEO starts with data. The first step is to perform a complete financial audit — every loan, every interest rate, every recurring expense. The goal is total visibility.

Phase 2: Strategic Planning

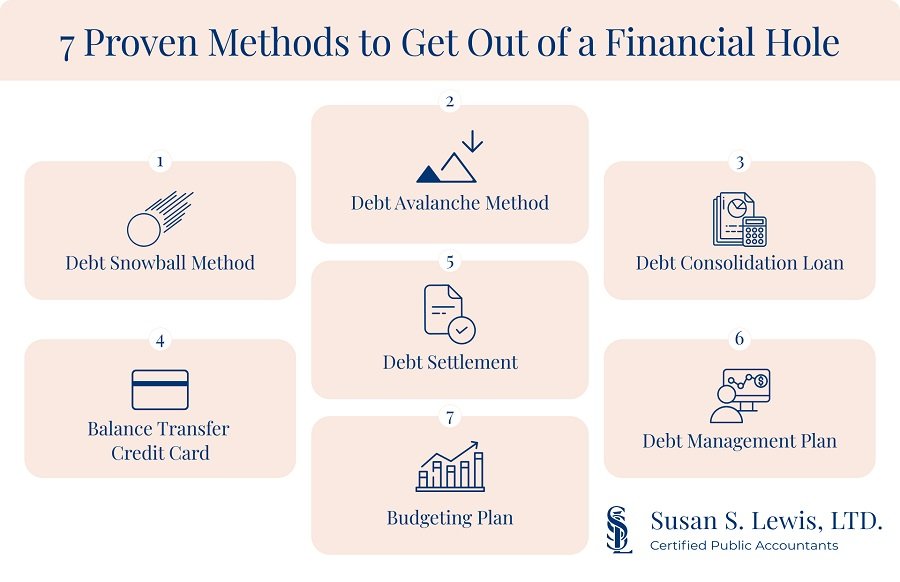

-Once the data is clear, the strategy begins. Choose between:

The Avalanche Method: Prioritize highest interest debts first for maximum savings.

The Snowball Method: Start with smallest debts for faster psychological wins.

The right method depends on one’s psychology — rational or emotional motivation.

Phase 3: Execution and Automation

-Manual budgeting often fails due to human error and inconsistency. Automation removes temptation and ensures reliability. Set up automatic payments, savings transfers, and alerts.

Phase 4: Review and Optimization

-Just like quarterly reviews in business, personal finance requires scheduled check-ins. Track progress, reassess priorities, and adapt to changing income or expenses.

Phase 5: Growth and Investment

-Debt elimination is not the end — it’s the beginning. Once free from debt, the next goal is wealth creation. Reinvest saved funds into assets, education, or entrepreneurship.

- The CEO Mindset: Running Your Life Like a Business

-Leaders thrive on structure, accountability, and measurable goals. The same principles apply to personal finance. When you adopt a CEO mindset, you begin to:

Treat your income as revenue.

Manage your spending as operating expenses.

Build reserves as your emergency fund.

Use ROI thinking to evaluate every financial decision.

This mindset transforms debt elimination from a chore into a business strategy. Every payment becomes an investment in future liquidity and freedom. Every sacrifice becomes a reinvestment in one’s own company — You Inc.

True leadership begins with self-mastery, and there is no greater form of mastery than control over one’s own finances. - Case Study: From Debt to Discipline

-Consider Sarah, a 32-year-old marketing manager burdened by $25,000 in credit card debt. Despite earning well, her spending habits kept her trapped in a cycle of minimum payments. When she adopted the “A Tool To Eliminate Debt” framework, everything changed.

First, she mapped her debts and confronted the full picture — a moment of accountability many avoid. Then she implemented the avalanche method, focusing on high-interest cards. She automated her payments and used visual progress dashboards to track improvement.

In 18 months, she became debt-free. But more importantly, her mindset shifted. She no longer saw budgeting as restriction — but as empowerment. Today, Sarah saves 20% of her income monthly and has launched a side business.

Debt elimination wasn’t her end goal — it was her launch pad. - Leadership Lessons from Debt Management

-For CEOs and entrepreneurs, personal financial discipline often reflects in organizational performance. Leaders who manage their personal finances with clarity and control tend to run more efficient, resilient companies.

From debt elimination, executives can extract key leadership lessons:

Transparency Builds Trust: In finance and in leadership, honesty with oneself is the foundation of progress.

Small Wins Drive Momentum: Progress, not perfection, keeps teams (and individuals) motivated.

Automation Reduces Risk: Delegation and systems outperform willpower — in business and in budgeting.

Data Drives Decisions: Objective analysis leads to better outcomes than emotion-driven choices.

Long-Term Thinking Wins: Both in business strategy and debt elimination, patience compounds into success. - The Cultural Shift Toward Financial Empowerment

-We are witnessing a cultural evolution in how people view debt. For generations, debt was a private shame — a personal secret. Today, transparency, education, and technology are rewriting that narrative. Financial literacy is becoming a leadership skill, not a personal topic to avoid.

A Tool To Eliminate Debt is not just about paying bills; it’s about restoring dignity, confidence, and autonomy. When individuals are financially free, they think more creatively, work more passionately, and lead more effectively.

Imagine a world where every employee, entrepreneur, and executive operates without the burden of personal debt — where financial clarity fuels innovation rather than fear. That is not just an economic goal; it’s a human one. - The Future of Personal Finance: Intelligence + Empathy

-The next frontier in debt elimination is AI-powered financial coaching — intelligent systems that combine analytics with empathy. Unlike traditional banks that profit from debt, new financial technologies are being built to help people eliminate it.

Such tools will understand spending behavior, predict financial stress, and offer personalized strategies. They will be proactive, not reactive — preventing debt before it begins. This is the digital transformation of personal finance — data-driven, ethical, and empowering.

But technology will never replace the human element. True financial transformation comes from self-awareness, consistency, and purpose. The best tool in the world means nothing without the discipline to use it. - The Human Side of Financial Freedom

-Eliminating debt is not only about numbers — it’s about emotions, relationships, and identity. Debt often brings shame, anxiety, or isolation. Conversely, financial freedom brings confidence, security, and peace of mind.

A Tool To Eliminate Debt helps individuals rewrite their story. It restores a sense of control. It empowers people to dream again, plan again, and build again — without the invisible chains of financial pressure.

At its heart, this tool is about liberation. Because when a person becomes debt-free, they don’t just gain money — they regain time, choice, and possibility. - Conclusion: Leading the Future of Financial Empowerment

-Debt elimination is not a trend — it is a revolution in personal responsibility and human potential. The world does not need more financial products; it needs smarter, simpler systems that empower people to manage what they already have wisely.

As leaders, we have a moral and strategic duty to encourage financial literacy — within our organizations, our families, and ourselves. When people control their finances, they control their futures. And when that happens on a large scale, societies become stronger, economies become more resilient, and innovation flourishes.

A Tool To Eliminate Debt is not just an app, a method, or a theory. It is a vision for a new kind of prosperity — one built not on consumption, but on clarity; not on loans, but on leadership.

Debt freedom is not the end of the story. It is the beginning of a life lived with purpose, confidence, and control.

Final Word

-True success is not measured by income alone, but by autonomy — the ability to make choices without financial fear. Debt may be the most common obstacle in the modern world, but with the right mindset, structure, and tools, it is also one of the most solvable.

It begins with awareness. It thrives on discipline. And it ends in freedom.

That is the promise — and the power — of A Tool To Eliminate Debt.

Title:

0% APR Credit Cards: A Tool To Eliminate Debt

Word Count:

494

Summary:

It is interesting to note that what started off as a marketing gimmick has now become an almost permanent part of the credit card industry in America and today 0% APR credit cards can in fact play a significant role in helping a person reduce or get out of debt.

What Is A 0% APR Credit Card?

APR is the annual interest rate known in industry jargon as the Annual Percentage Rate. It is a reflection of the cost of credit. In the old days everybody paid a standard APR based…

Keywords:

0 apr credit card, 0 apr, credit card, balance transfer, interest free, offers, rate, reduce debt

Article Body:

It is interesting to note that what started off as a marketing gimmick has now become an almost permanent part of the credit card industry in America and today 0% APR credit cards can in fact play a significant role in helping a person reduce or get out of debt.

What Is A 0% APR Credit Card?

APR is the annual interest rate known in industry jargon as the Annual Percentage Rate. It is a reflection of the cost of credit. In the old days everybody paid a standard APR based on bank rates. It was usually about 18 per cent. The use of low APR came with the emergence of the monoline bank. These were banks that only issued credit cards and did not take any deposits or issue conventional loans. For their business model to work well large numbers were important for these breed of pioneering bankers and credit cards issuers so low APR teaser rates were successfully used to lure as many new card users as possible.

The gimmick seemed to have worked so well that today it is difficult to find a credit card company that does not offer some type of incentive APR during the first 6 months or one year. The more popular credit cards offer 0% APR for the first year.

Usefulness Of A 0% APR Credit Card In Reducing Debt

A 0% APR credit card can be extremely useful for somebody who wants to reduce their large credit card debt. For instance if you have a credit card debt that remains at about $10,000 and the APR is 20% then you will end up paying a whooping $2,000 in interest payments alone. With a 0% APR credit card the $2,000 could all go towards reducing that crippling debt. It is therefore clear that 0% APR credit cards can offer much needed financial breathing room for somebody in a serious credit card debt situation.

Consolidation Or Transfer Necessary To Benefit From 0% APR Credit Cards

Transferring a credit card debt or credit card debt consolidation are all-important first steps that will need to be taken before a person in deep credit card debt can enjoy the benefits of a 0% APR credit card. The objective here would be to have all the person�s outstanding debt payable to one credit card company and at a 0% APR rate.

The importance of 0% APR credit cards in helping an individual or business to get out of credit card debt cannot be understated.

Although many potential card users place a lot of importance in being able to obtain a 0% APR credit card, the truth of the matter is that it is only attractive and beneficial to two groups of people. Firstly persons able to settle their credit card balances on a month to month basis to whom the 0% APR rate means that their cost of maintaining a credit card is very minimal. Secondly those in debt also benefit because the 0% APR credit card greatly assists them in their efforts to reduce their debt.

Copyright 2005 Ed Vegliante.

Tinggalkan Balasan